-

Global air cargo tonnages rose by 5 percent year-on-year in November, with Southeast Asia to US volumes surging by 42 percent while flows from China and Hong Kong to the US dropped by 8 percent.

-

Air cargo rates climbed 7 percent month-on-month to US$2.65/kg in November, with strong price gains from Central & South America and Asia Pacific origins, despite spot rates still 5 percent below last year’s level.

-

Year-to-date data confirms a trade shift: tonnages from China and Hong Kong to Europe are up 8 percent, while Southeast Asia–US volumes soared 27 percent, reflecting sourcing shifts amid tariff and regulatory changes.

Worldwide air cargo tonnages in November continued their year-on-year (YoY) growth pattern with a 5 percent increase, slightly widening the YoY growth from the 4 percent recorded in October and September, indicating solid YoY growth in Q4 so far.

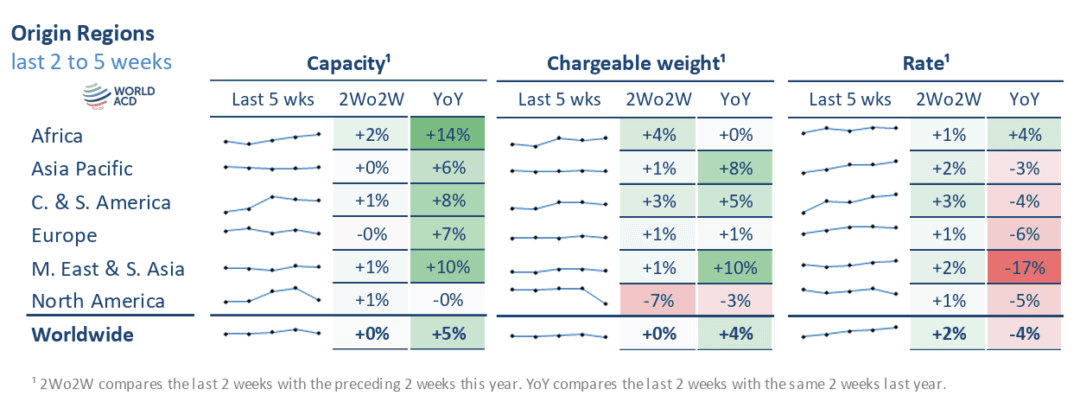

According to the latest weekly figures and analysis from WorldACD Market Data, that growth was led, in percentage terms, by YoY increases in traffic from Middle East & South Asia (MESA, 11 percent), Asia Pacific (8 percent), and Central & South America (CSA, 6 percent) origins, although in absolute terms the biggest factor was the YoY increase in cargo from Asia Pacific origins.

A month-on-month (MoM) comparison shows a 3 percent higher average worldwide volume per week in November compared with October, with Asia Pacific (5 percent) and CSA (6 percent) the two origin regions showing significant MoM growth. MESA (3 percent) and Africa (2 percent) were also up, while there were slight decreases from North America (minus 2 percent) and Europe (minus 1 percent).

Southeast Asia to US boom

Looking specifically at the key Asia Pacific origin markets, further analysis by WorldACD – based on the more than two million monthly transactions covered by its data – reveals a mixed picture characterised by the contrasting performances of key markets to the US and to Europe. For example, tonnages from Asia Pacific to the US were up by around 6 percent, YoY, in November, but most of that was generated by growth from Southeast Asia origins to the US, whereas there were decreases from China & Hong Kong (CN/HK), Japan, and South Korea to the US.

Combined tonnages from China & Hong Kong to the US in November were down YoY by 8 percent, with China to US volumes down by 5 percent and Hong Kong to US chargeable weight dropping by 14 percent. In contrast, from Southeast Asia, tonnages were up by around 42 percent YoY to the US. That reflects a clear pattern among US importers sourcing products from alternative production markets in Asia in response to increased tariffs on US imports from China and the removal of ‘de minimis’ exemptions.

Contrasting US vs Europe patterns

Equally notable is the comparison between the traffic patterns to Europe and the US. Combined tonnages from CN/HK to Europe were up by 8 percent in November YoY, directly contrasting with the 8 percent drop from CN/HK to the US. Separate figures show China exports to Europe up more than 5 percent in November, while China to US tonnages fell by 5 percent. From Hong Kong to Europe, volumes were up by 14 percent, in stark contrast to the 14 percent drop to the US.

These figures reflect a shift in air cargo tonnages and capacity from China and Hong Kong to European markets rather than to US markets. Year-to-date (YtD) figures for the first 11 months reinforce this trend: CN/HK tonnages to the US are down by 7 percent, while volumes to Europe are up by 8 percent YoY.

Year-to-date tonnages from Southeast Asia to the US are up by 27 percent, whereas to Europe they are down by 5 percent, highlighting a strong divergence in the performance of these major trade lanes in 2025.

Rates continued to rise

On the pricing side, average worldwide rates in November stood at US$2.65 per kilo – based on a mix of spot and contract rates – up by 7 percent compared with October’s levels. This was a stronger MoM increase than the 5 percent seen this time last year. The biggest MoM percentage increases in average rates were from CSA (9 percent) and Asia Pacific (8 percent) origins.

Spot rates followed a similar pattern, with a 7 percent MoM rise to US$2.87 per kilo, led by increases from CSA (10 percent), Asia Pacific (9 percent), and Europe (9 percent). However, overall global average spot rates were 5 percent below their level last November. Spot rates declined YoY from all major origin regions apart from Africa (up 6 percent YoY), with the steepest drop from MESA origins, where spot prices were 26 percent lower than in November 2024.

On a year-to-date basis, worldwide average rates of US$2.45 per kilo were virtually unchanged from last year’s equivalent of US$2.46.

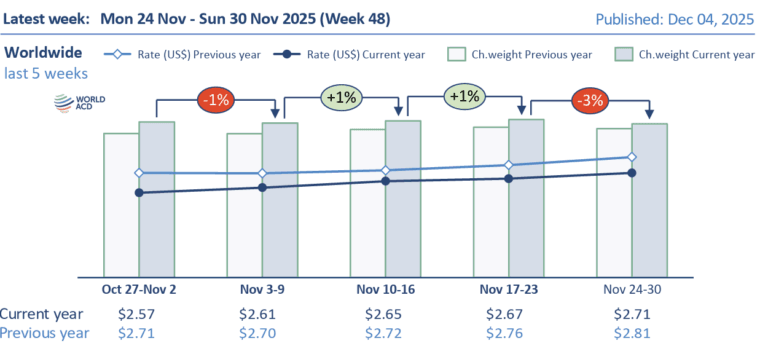

Week 48 trends

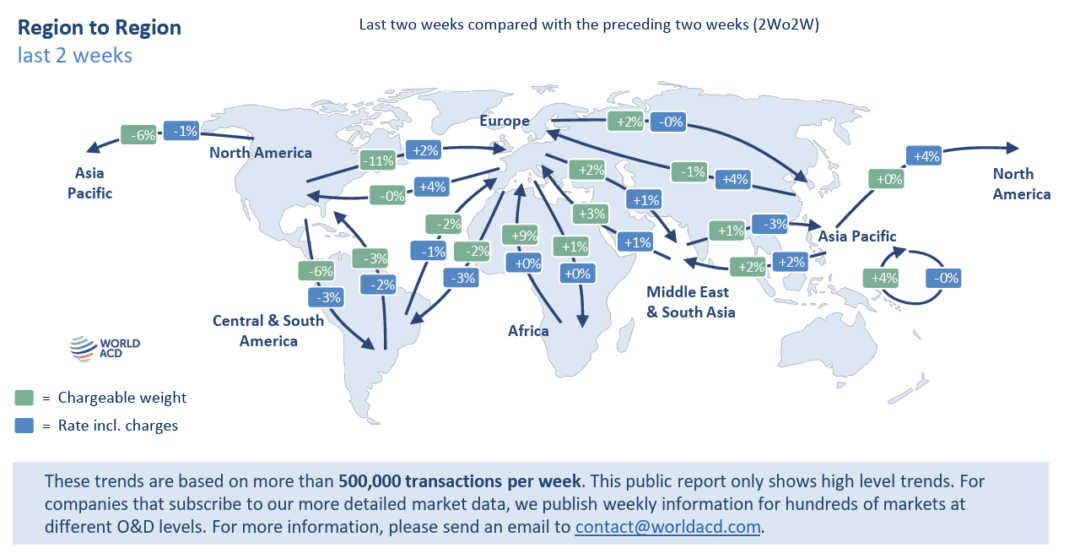

In week 48 (24 to 30 November), volumes dipped by 3 percent week-on-week (WoW), mostly due to the impact of the Thanksgiving holiday in the US, which saw ex-North America volumes drop by 15 percent WoW. Excluding this, volumes from other origin regions fell just 1 percent WoW, reflecting mild declines from MESA (2 percent), CSA (2 percent), and Europe (1 percent), while Asia Pacific remained almost flat.

Average worldwide rates rose again by 1 percent WoW – a trend typical for this time of year – while the YoY rate gap remained stable at minus 4 percent. Spot rates climbed 3 percent WoW to US$2.96 per kilo, with increases from MESA (3 percent), and 2 percent rises from Asia Pacific, Europe, and CSA, partially offset by declines from North America (minus 11 percent) and Africa (minus 4 percent). Overall, average worldwide spot rates stood 6 percent below their level in the equivalent week of 2024.